osptm = matrix(c(0.7,0.1,0.2, 0,0.6,0.4, 0.5,0.2,0.3), nrow = 3, byrow = TRUE)

osptm [,1] [,2] [,3]

[1,] 0.7 0.1 0.2

[2,] 0.0 0.6 0.4

[3,] 0.5 0.2 0.3This post is an introduction to Markov Chain with a presentation of Discrete Time Markov Chains.

A stochastic process is \(\{ X(t), t \in T \}\) is a collection of random variables indexed by a parameter t that belongs to a set T.

A discrete-time Markov Chain is a discrete-time stochastic process which state space S is finite such that: \[\mathbb{P}(X_{n+1} = j | X_0 = i_0, X_1 = i_1, X_2 = i_2, \dots, x_n = i) = \mathbb{P}(X_{n+1} = j | X_n = i) = P_{ij}\]

that is, the conditional probability of the process being in state j at time n + 1 given all the previous states depends only on the last-known position (state i at time n).

We denote the probability to go from state \(i\) to state \(j\) in n-steps by \(\bf{P}_{ij}^{(n)}\). It is also denoted as the n-steps transition probability matrix. That is for any time \(m >= 0, \bf{P}_{ij}^n = \mathbb{P}(X_{m+n} = j | X_m = i)\) . \(\bf{P}^{(n)} = \bf{P}^n\) based on the Chapman-Kolmogorov equation.

The Chapman-Kolmogorov equation states that for all positive integers \(m\) and \(n\) , \(\bf{P}^{(m+n)} = \bf{P}^m \cdot \bf{P}^n\) where P is a one-step probability transition matrix (a square matrix)

To model a Markov Chain, let’s first set up a one-step probability transition matrix (called here osptm).

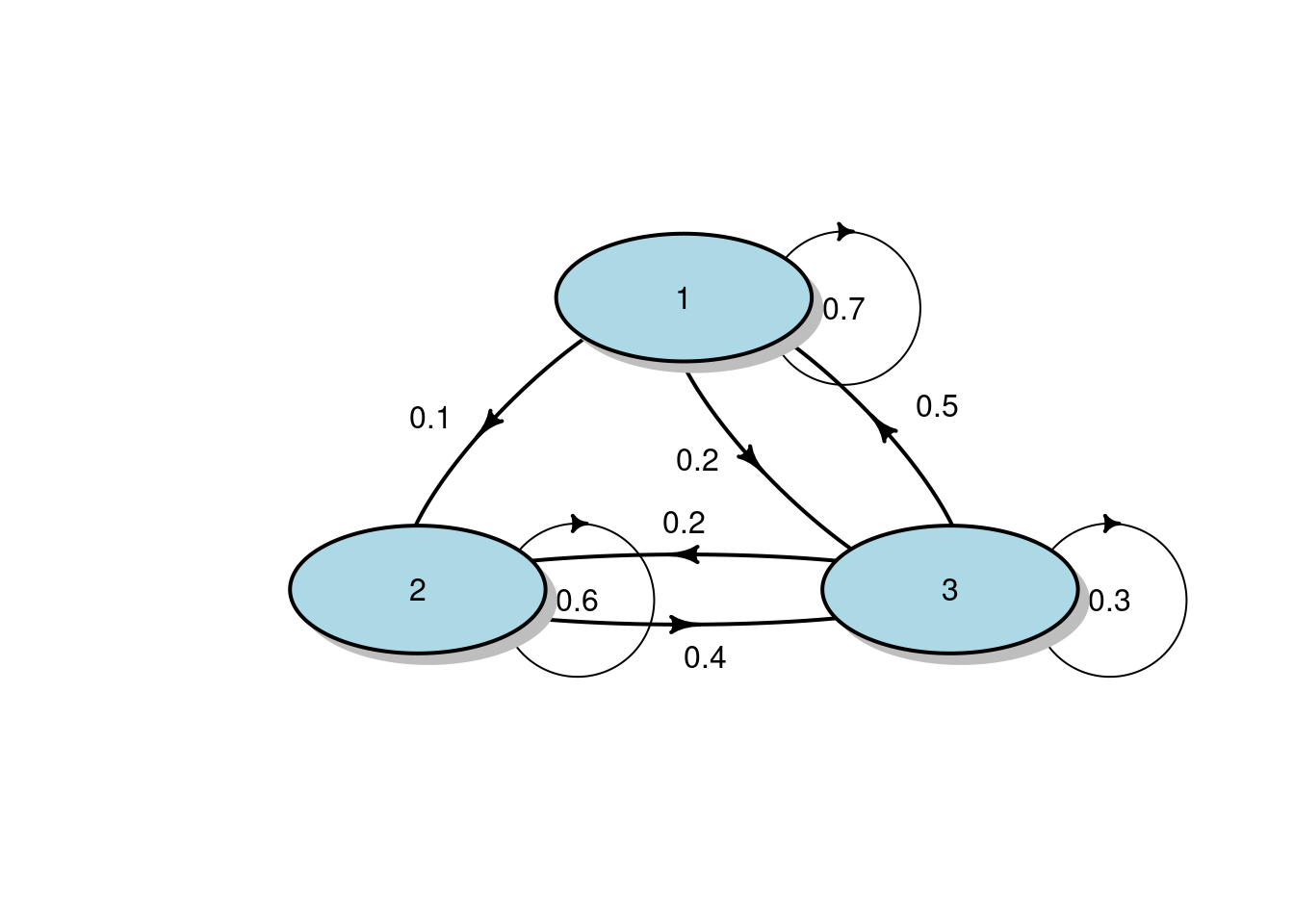

We start with an easy 3 possible state process. That is the state space \(S = \{1, 2, 3\}\). The osptm will provide the probability to go from one state to another.

osptm = matrix(c(0.7,0.1,0.2, 0,0.6,0.4, 0.5,0.2,0.3), nrow = 3, byrow = TRUE)

osptm [,1] [,2] [,3]

[1,] 0.7 0.1 0.2

[2,] 0.0 0.6 0.4

[3,] 0.5 0.2 0.3We can always have a look at how the osptm looks like.

# note we have to transpose the osptm matrix first.

osptm_transposed = t(osptm)

osptm_transposed [,1] [,2] [,3]

[1,] 0.7 0.0 0.5

[2,] 0.1 0.6 0.2

[3,] 0.2 0.4 0.3diagram::plotmat(osptm_transposed, pos = c(1, 2), arr.length = 0.3,

box.col = "lightblue", box.prop = 0.5, box.size = 0.12, box.type="circle",

self.cex = 0.6, self.shifty=-0.01, self.shiftx = 0.15)

The markovchain package can provide us with all the state characteristics of a one-step probabilty transition matrix.

library(markovchain)

osptm_mc <- new("markovchain", transitionMatrix = osptm)

recurrentClasses(osptm_mc)[[1]]

[1] "1" "2" "3"transientClasses(osptm_mc)list()absorbingStates(osptm_mc)character(0)period(osptm_mc)[1] 1round(steadyStates(osptm_mc), 4) 1 2 3

[1,] 0.4651 0.2558 0.2791The next step is to calculate, for instance, what is the probability to go from state 1 to state 3 in 4 steps.

library(expm)

# the expm library brings in the " %^%" operator for power.

osptm %^% 4 [,1] [,2] [,3]

[1,] 0.5021 0.2303 0.2676

[2,] 0.3860 0.3104 0.3036

[3,] 0.4760 0.2483 0.2757Looking at the result, we can see that the probability to go from State 1 to State 3 in 4 steps is 0.2676

We can also calculate the unconditional distribution after 4 steps

initial_pro <- c(1/3, 1/3, 1/3)

initial_pro %*% (osptm %^% 4) [,1] [,2] [,3]

[1,] 0.4547 0.263 0.2823Using a slightly more interesting one-step probability transition matrix having 6 different states.

#specifying transition probability matrix

osptm<- matrix(c(0.3,0.7,0,0,0,0,1,0,0,0,0,0,0.5,0,0,0,0,0.5, 0,0,0.6,0,0,0.4,0,0,0,0,0.1,0.9,0,0,0,0,0.7,0.3), nrow=6, byrow=TRUE)

osptm [,1] [,2] [,3] [,4] [,5] [,6]

[1,] 0.3 0.7 0.0 0 0.0 0.0

[2,] 1.0 0.0 0.0 0 0.0 0.0

[3,] 0.5 0.0 0.0 0 0.0 0.5

[4,] 0.0 0.0 0.6 0 0.0 0.4

[5,] 0.0 0.0 0.0 0 0.1 0.9

[6,] 0.0 0.0 0.0 0 0.7 0.3osptm_transposed = t(osptm)

diagram::plotmat(osptm_transposed, arr.length = 0.3, arr.width = 0.1,

box.col = "lightblue", box.prop = 0.5, box.size = 0.09, box.type="circle",

cex.txt = 0.8, self.cex = 0.6, self.shifty=-0.01, self.shiftx = 0.13)

osptm_mc <- new("markovchain", transitionMatrix = osptm)

recurrentClasses(osptm_mc)[[1]]

[1] "1" "2"

[[2]]

[1] "5" "6"transientClasses(osptm_mc)[[1]]

[1] "3"

[[2]]

[1] "4"absorbingStates(osptm_mc)character(0)period(osptm_mc)Warning in period(osptm_mc): The matrix is not irreducible[1] 0round(steadyStates(osptm_mc), 4) 1 2 3 4 5 6

[1,] 0.0000 0.0000 0 0 0.4375 0.5625

[2,] 0.5882 0.4118 0 0 0.0000 0.0000We can see that there are 2 possible steady states. Hence the Markov Chain is non-ergodic.